Despite the fact that we have no listed options on cryptocurrencies yet (Feb 2018), it would be interesting to calculate their theoretical Fair Values. In fact, it is quite an easy task since we have a series of historical quotes of an underlying cryptocurrency.

According to the OptionSmile methodology, we just need to build a probability distribution of historical returns and then, for any given expiration/moneyness, calculate the probability of in-the-money expiration (Pitm) and conditional expected value (payoff) in such expirations (EVitm).

That is just a theoretical exercise, of course, without a practical application. Not only due to the absence of an opportunity to trade these contracts but also because of the huge diversity of market regimes that took place in the past for these assets. Combining together the prolonged periods of extreme uptrends and the following crashes will inevitably produce a mixed bag of regimes that will have quite a poor prediction power.

Nevertheless, it is still interesting to look at the results in comparison with the regular, more mature instruments like stocks and ETFs. Just for the sake of curiosity.

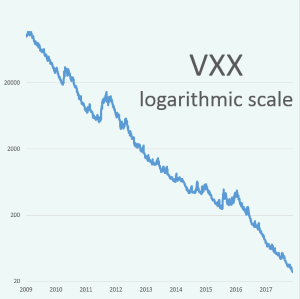

iPath S&P 500 VIX Short-Term Futures exchange-traded note (VXX), as many other similar volatility products, has been initially designed to provide an exposure to the volatility index on S&P500 – VIX. Being included in the long-term investment portfolio, this ETN was supposed to serve as a safety buffer during the market drops and, hence, should decrease the overall portfolio volatility enhancing the risk-adjusted return.

However, since VIX itself is just an index and is not tradable, VXX employs futures on VIX to replicate the desired exposure, and this changes the internal mechanics of this product completely. It demonstrates the positive dynamics only in the short-term – in times of volatility splashes, but during all other, more silent, periods, it is exposed to another very strong factor – volatility term structure. That phenomenon reflects the expectation of the market about the future VIX levels and is captured by the futures on VIX traded on the CBOE Futures Exchange (CFE). Most of the time, the VIX futures are in a contango (the near future price is lower than the further), and VXX constantly diminishes its value by the negative daily “roll yield”.

In this research, we have compared four strategies to exploit the constant downtrend in VXX: buying the inverse VIX ETN – XIV and buying the put options on VXX with different strikes (OTM, ITM, and ATM).

Long Put strategies look appealing due to the inherent downside protection that, theoretically, could lead to the superior risk-adjusted returns. However, the conclusion we have come is that both buying XIV and puts on VXX have almost the same performance measures by the Sharpe ratio, maximum drawdowns, and the shape of equity curves.