Having broken up their trading ranges and all-time highs recently, all major equity indices do not demonstrate enough steam to move higher and seem to form another trading ranges instead. Volatility indices have been fluctuating around their normal levels of the recent months.

Options mispricing is back contrasting to the previous snapshot (September 4, 2018) when the most options series were priced fairly. The major changes happened in SPY and QQQ calls which flipped from the fairly priced to the substantial overpriced. The options market seems to estimate the further upward move as having very low probability.

Mispricing summary for the options with two to five weeks until expiration:

| Puts | Calls | ||||

| OTM | ATM | ATM | OTM | ||

| SPY |

2-3 weeks |

Overpriced |

Fairly priced |

Underpriced substantially |

|

|

4-5 weeks |

Overpriced substantially |

Overpriced |

Underpriced substantially | ||

| QQQ | 2-3 weeks |

Fairly priced |

Underpriced substantially | ||

|

4-5 weeks |

Overpriced |

Fairly priced |

Underpriced |

||

| IWM | 2-3 weeks | Overpriced | Fairly priced |

Fairly priced |

|

|

4-5 weeks |

Mixed |

Fairly priced |

Fairly priced |

||

Major opportunities can be found in overpriced puts on SPY, some OTM puts on QQQ and IWM, and calls on SPY and QQQ. Bullish risk reversals on SPY look attractive due to the substantial overpricing of puts combined with the underpricing of calls.

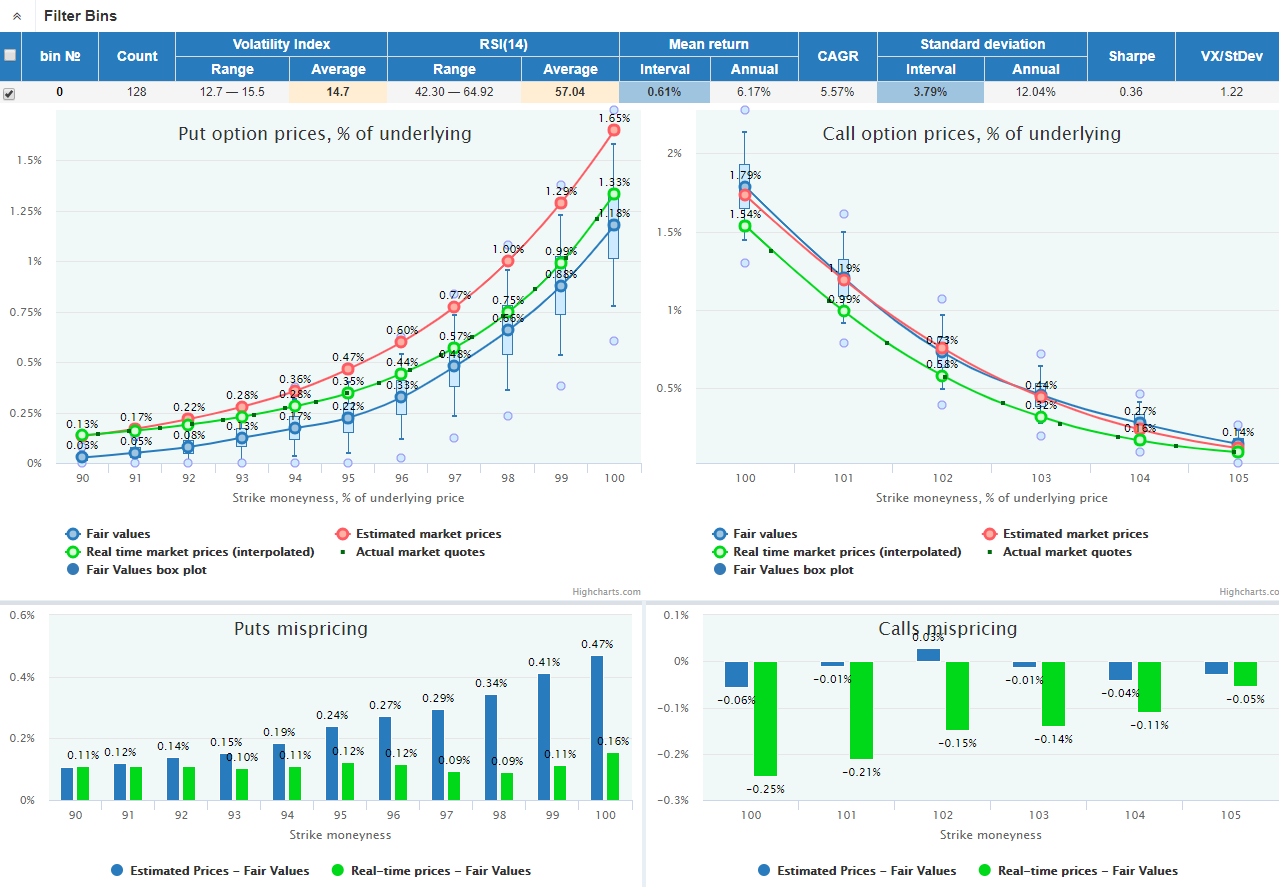

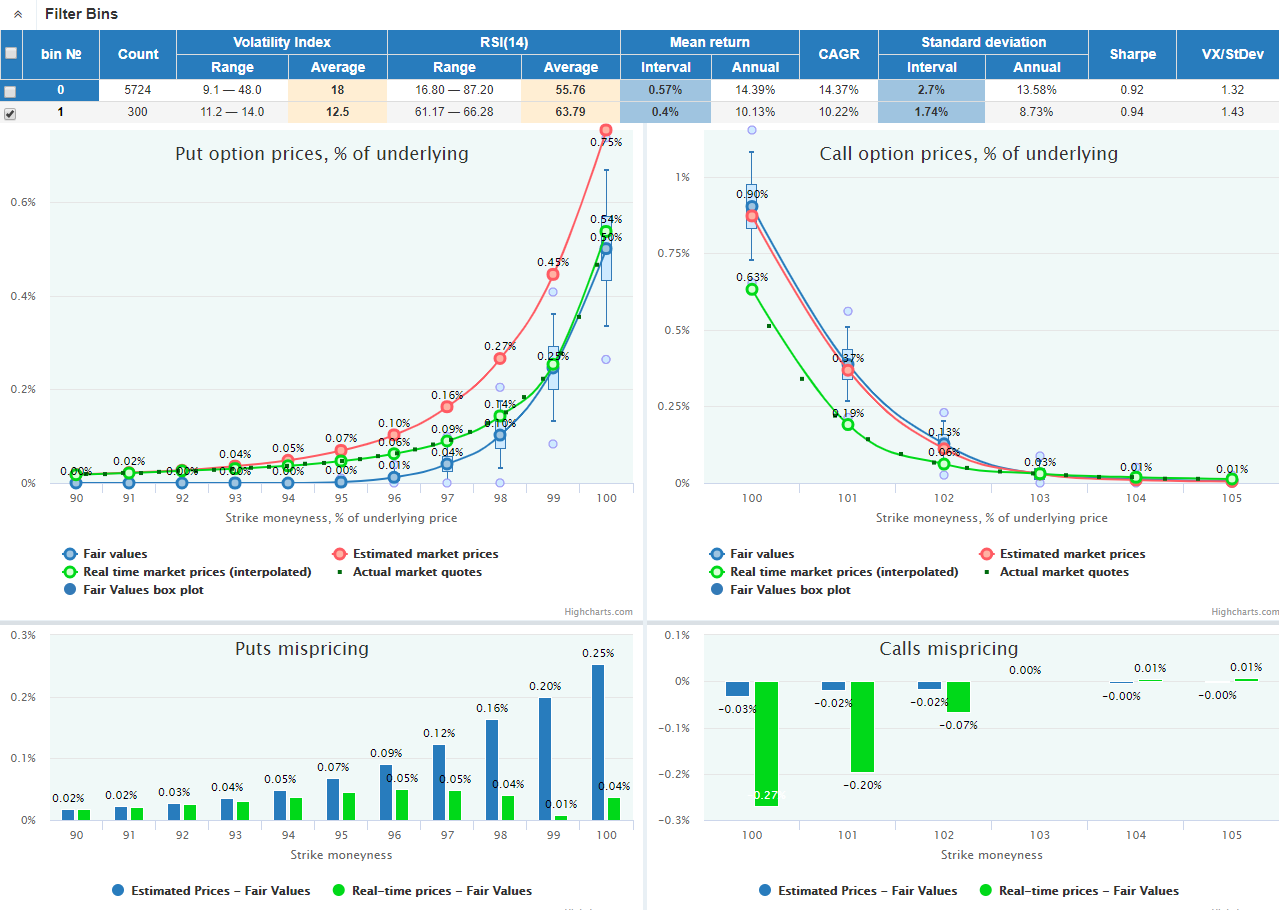

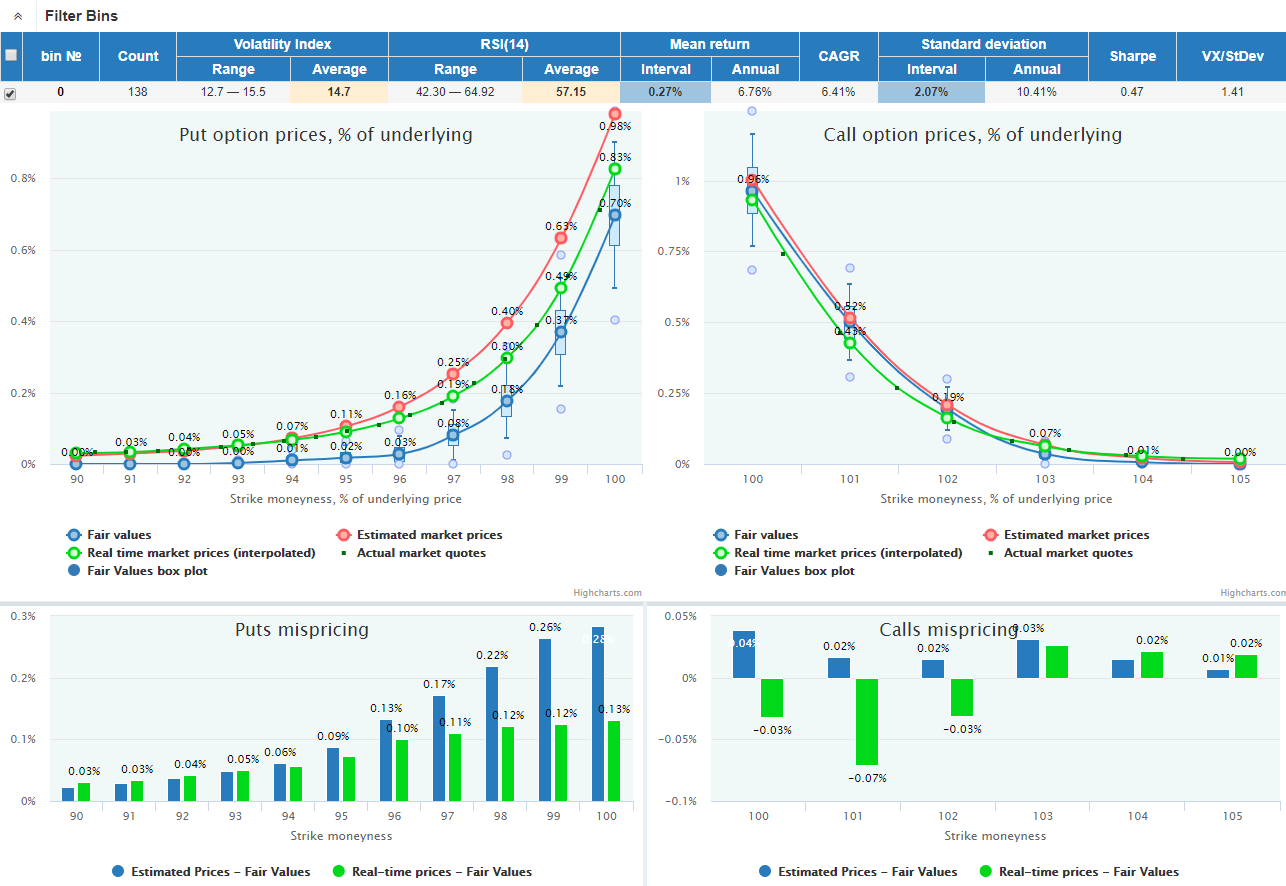

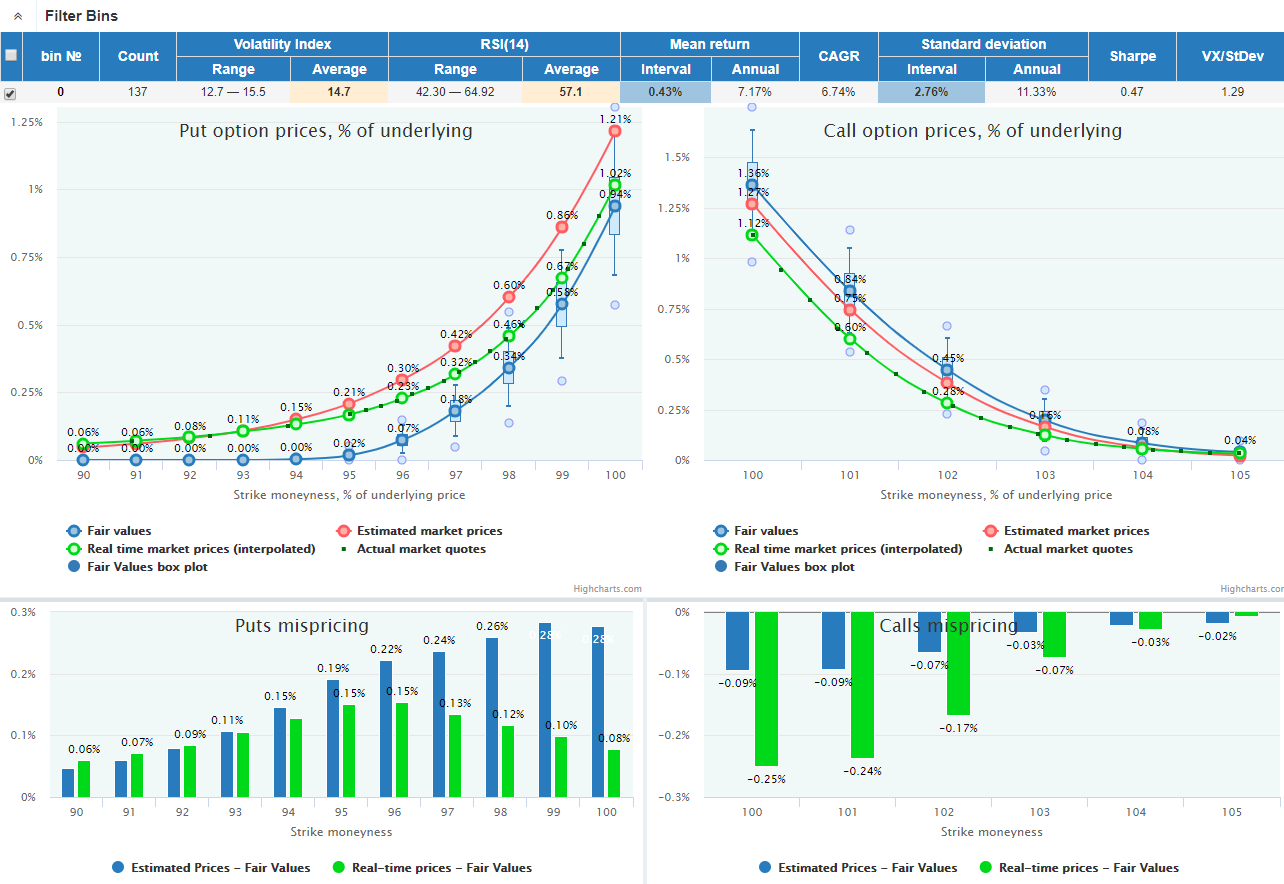

To make our estimation more reliable, we filter the historical data and select from the past only those dates when the market resembled the current condition (read more here). We use three filters:

For SPY and QQQ, we apply auto filtering for Volatility index and RSI selecting 300 days in history with the shortest Euclidean distance to their current values. For IWM, we use manual filtering since the current regime is not typical due to the relatively low implied volatility (RVX index).

For each underlying, we select expirations on a range of 2-5 weeks and present options Fair Values and Market Prices, both historical (red line) and current real-time (green line). The market prices of these two types can sometimes diverge from each other if the current market condition (volatility surface) differs from its average state in the history.

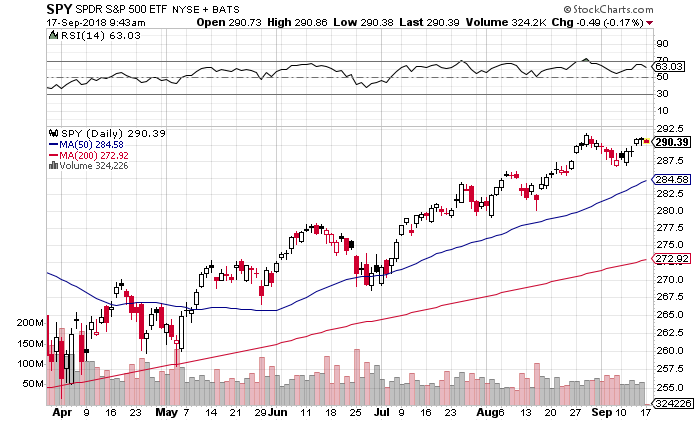

SPY has approached its all-time high again after a small correction in the last week; RSI(14) is in neither oversold nor overbought area.

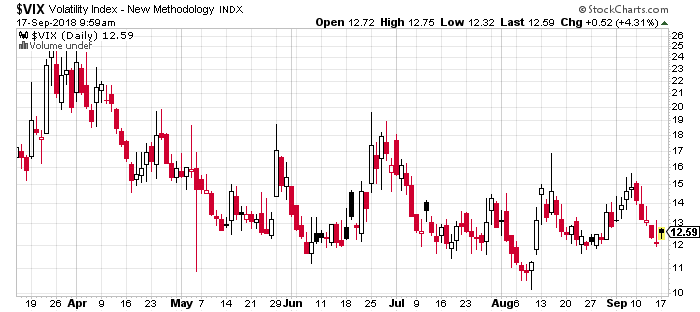

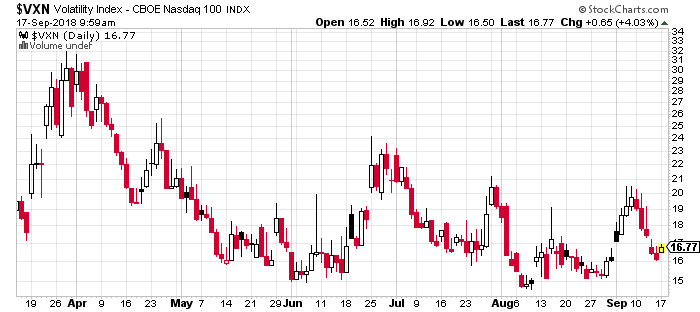

VIX got back to the lows of the recent months reflecting the silent market:

Puts are priced fairly; calls are underpriced. Market prices are adjusted for the September 21 dividend ($1.23).

OTM puts are overpriced; ATM puts are priced fairly; calls are substantially underpriced. Market prices are adjusted for the September 21 dividend ($1.23).

OTM puts are substantially overpriced; ATM puts are overpriced not significantly; calls are substantially underpriced. Market prices are adjusted for the September 21 dividend ($1.23).

Puts are substantially overpriced; calls are substantially underpriced. Market prices are adjusted for the September 21 dividend ($1.23).

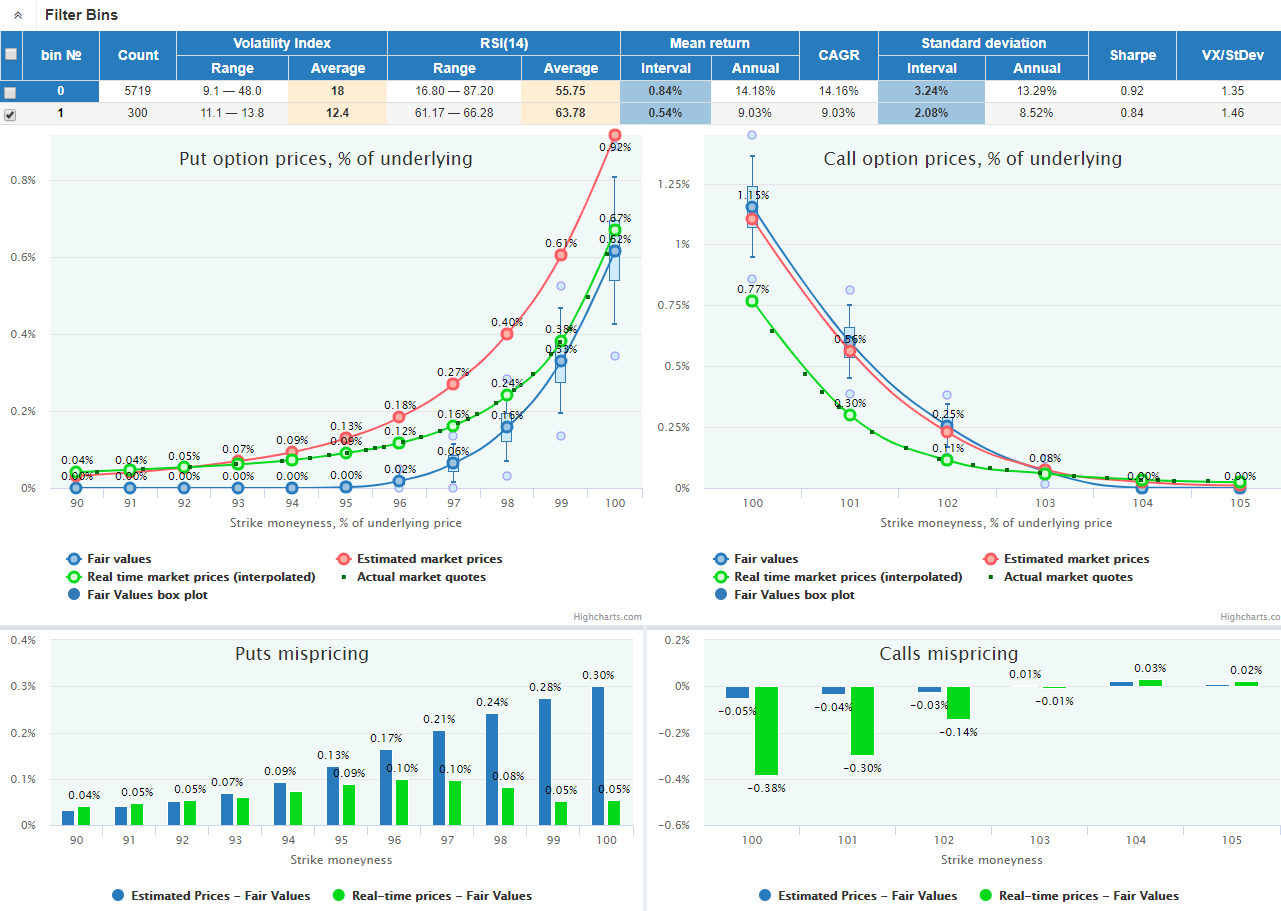

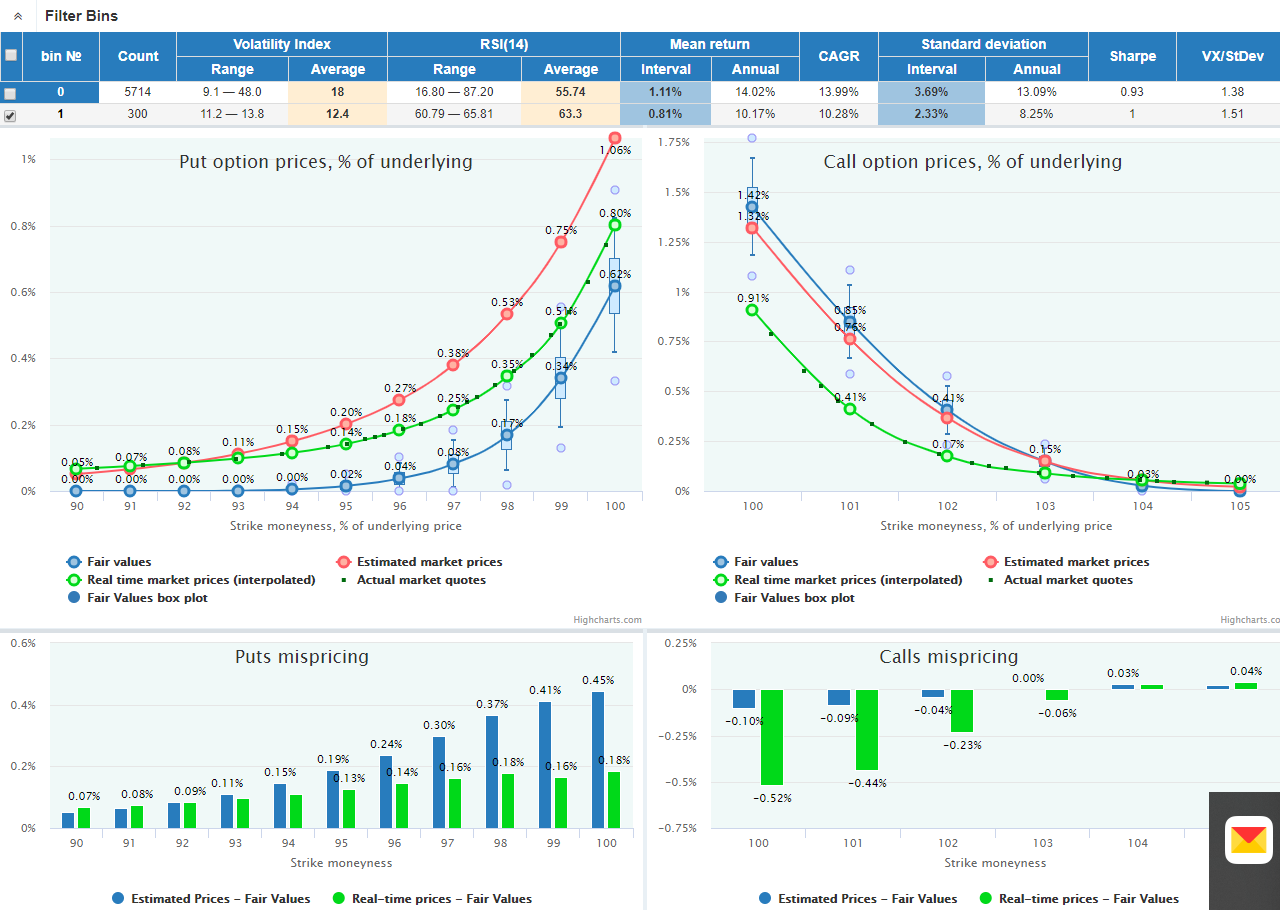

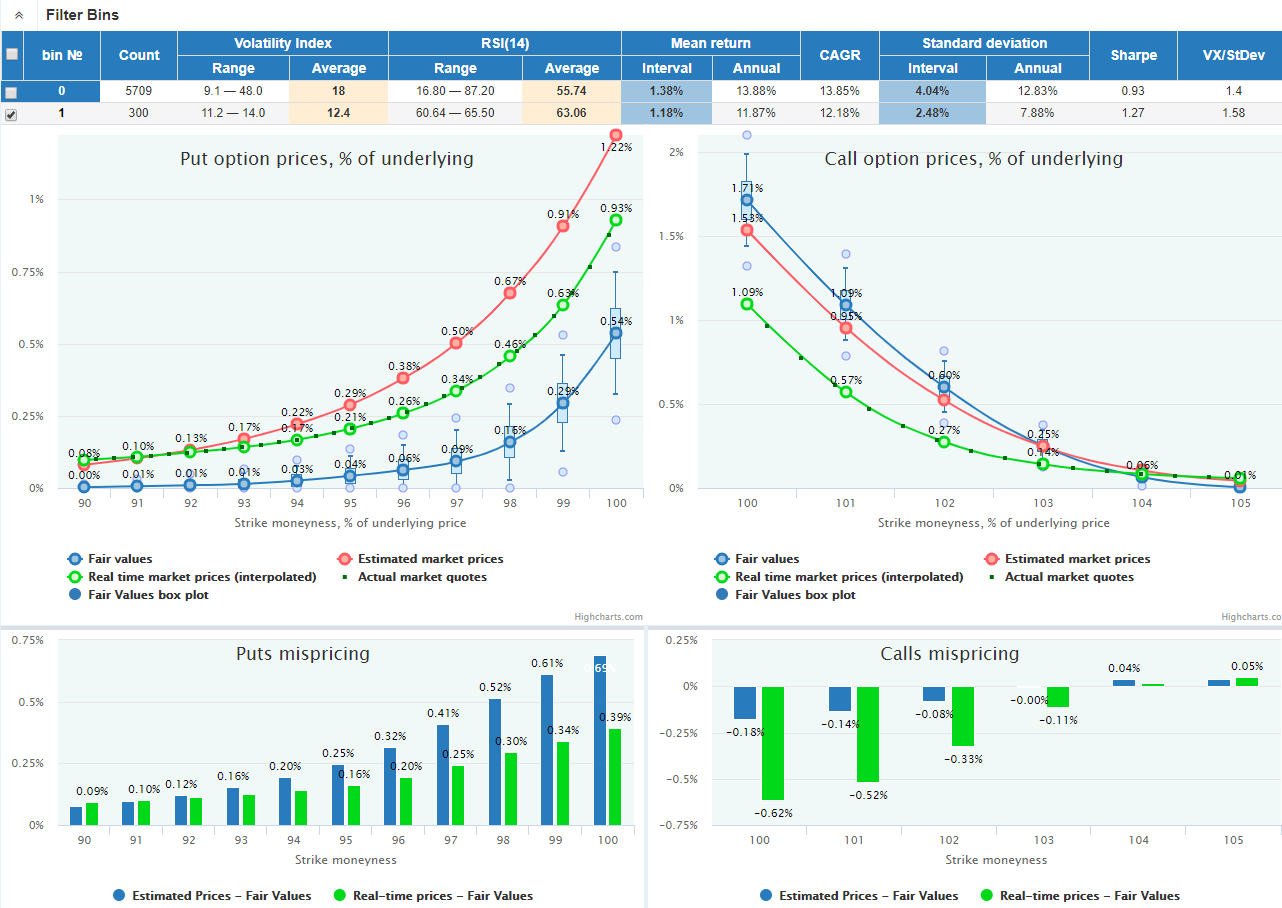

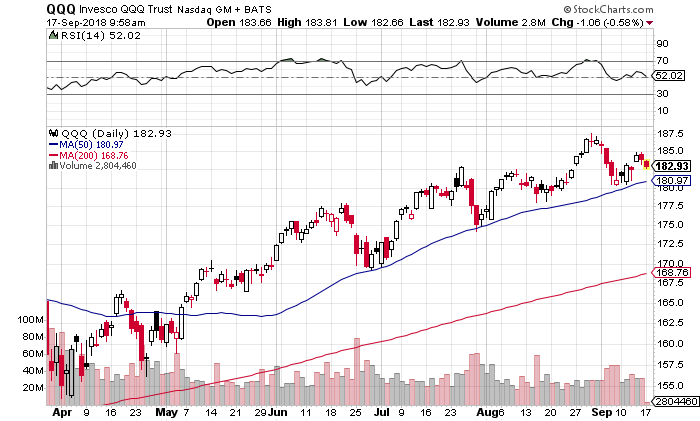

QQQ pulled back after the reaching its all-time high and looks like forming a new trading range; RSI(14) is fluctuating near the middle line of 50:

VXN demonstrates the silent market conditions overall:

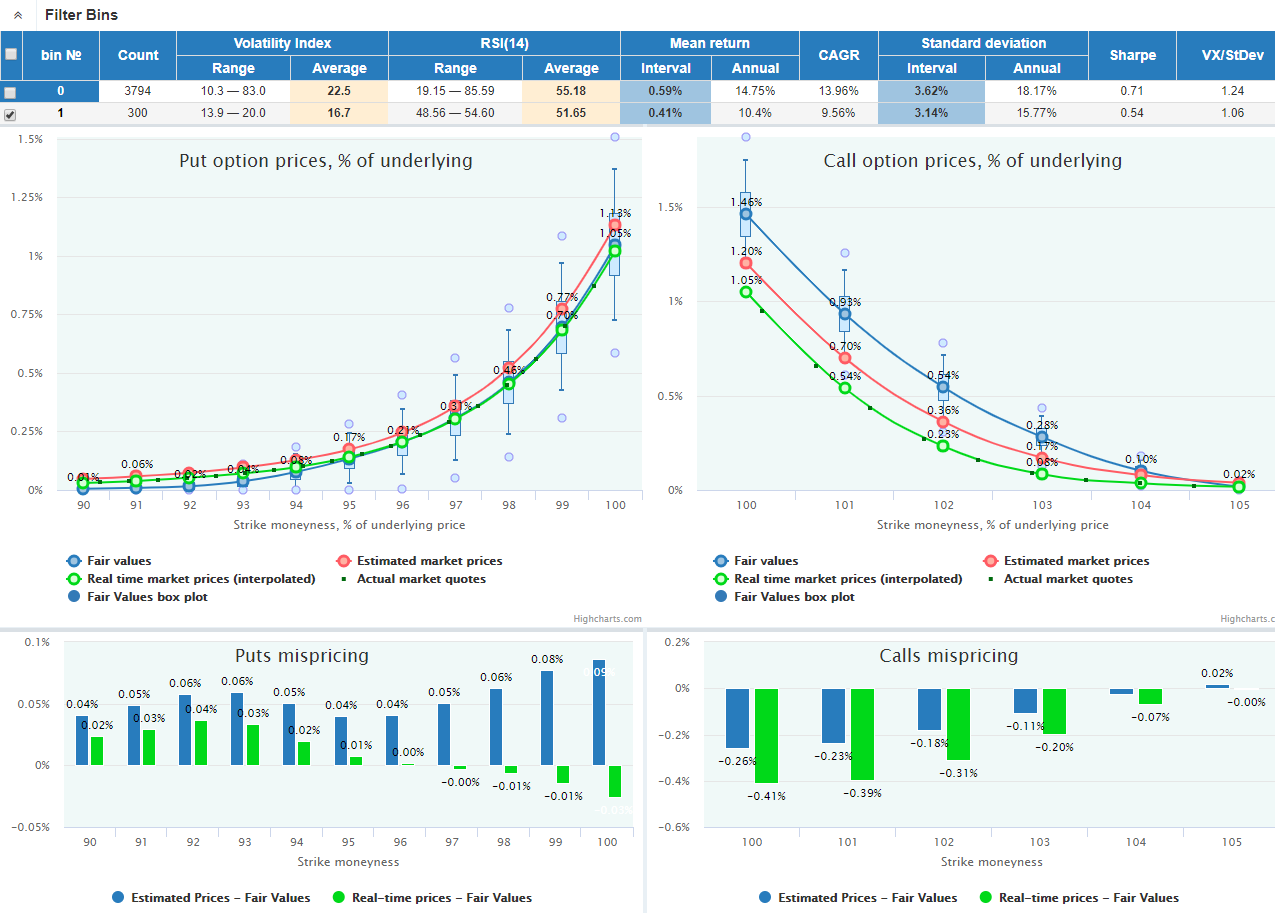

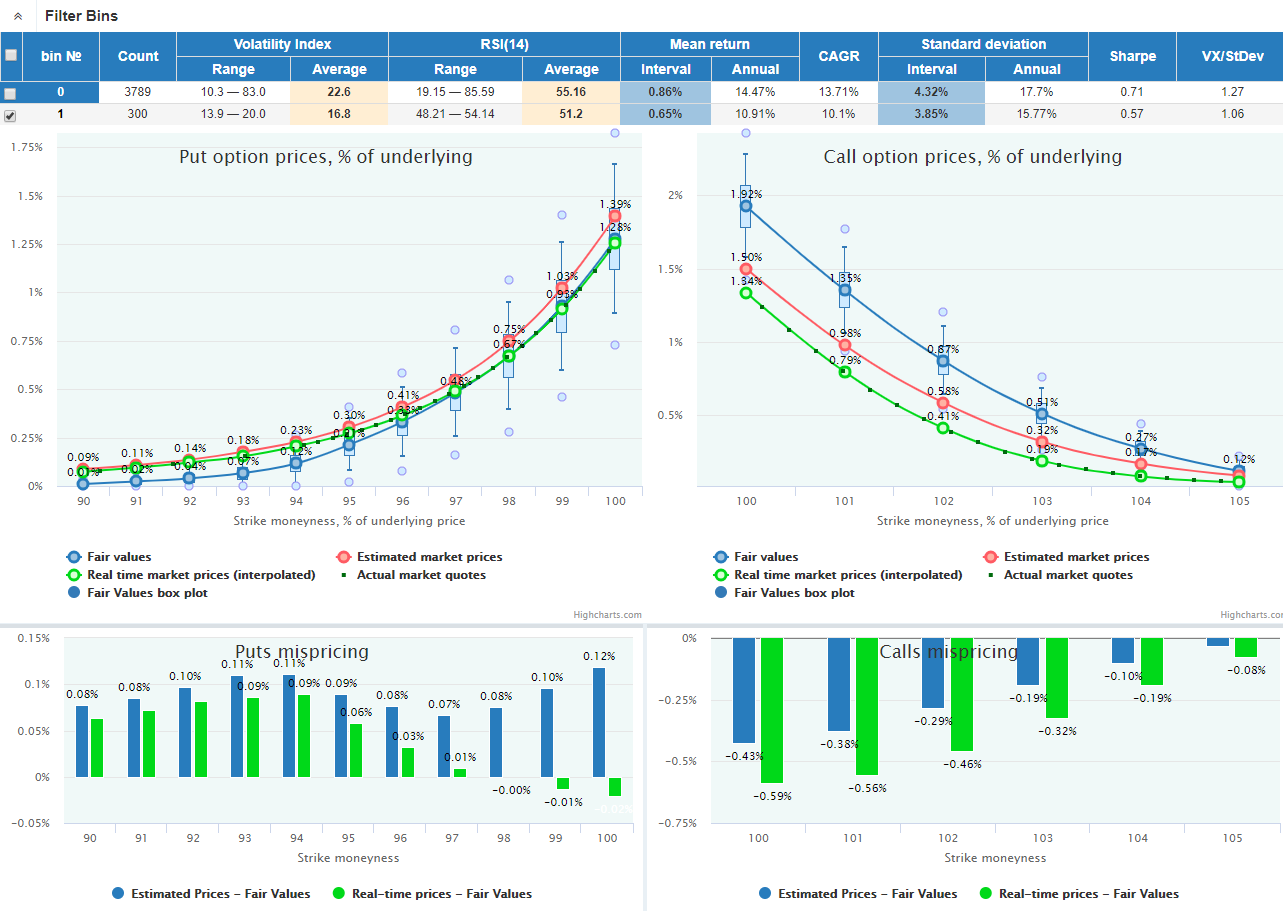

Puts are priced fairly; calls are substantially underpriced. Market prices are adjusted for the September 24 dividend ($0.308).

Puts are priced fairly; calls are substantially underpriced. Market prices are adjusted for the September 24 dividend ($0.308).

OTM puts are overpriced; ATM puts are priced fairly; calls are substantially underpriced. Market prices are adjusted for the September 24 dividend ($0.308).

OTM puts are overpriced; ATM puts are priced fairly; calls are underpriced. Market prices are adjusted for the September 24 dividend ($0.308).

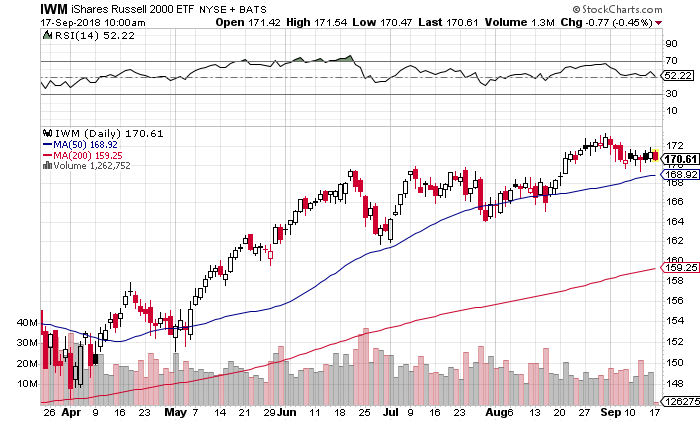

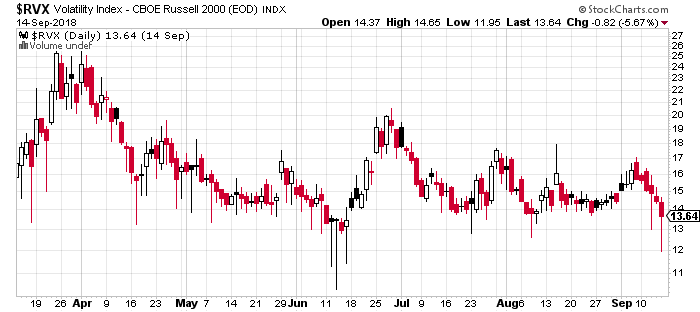

IWM has been hovering near the all-time high in the very narrow range; RSI(14) demonstrates neither overbought nor oversold conditions:

RVX is near its lows of the recent months reflecting the silent market conditions.

OTM puts are overpriced; ATM puts mispricing is not significant; calls are priced fairly. Market prices are adjusted for the September 26 dividend ($0.419).

OTM puts are overpriced; mispricing of calls and ATM puts is not significant. Market prices are adjusted for the September 26 dividend ($0.419).

OTM puts are substantially overpriced; ATM puts are priced fairly; calls are underpriced. Market prices are adjusted for the September 26 dividend ($0.419).

Both puts and calls are priced fairly. Market prices are adjusted for the September 26 dividend ($0.419).