Put options on broad-based equity indices are systematically overpriced as measured by the expected profit of buying or selling them. Market prices for put options are usually higher than their Fair Values because of the volatility premium demanded by option sellers as compensation for high volatility and the potential for huge drawdowns. For more information, see this research: Are puts really overpriced?

However, since an expected value (all possible outcomes weighted by their probabilities) is always calculated as an arithmetic average, options Fair Values and their respective expected profit/loss do not reflect the compounding effect of returns. At the same time, we know that drawdowns have a negative impact on the total return if we capitalize all gains and losses (volatility “drag”), see more information in this post.

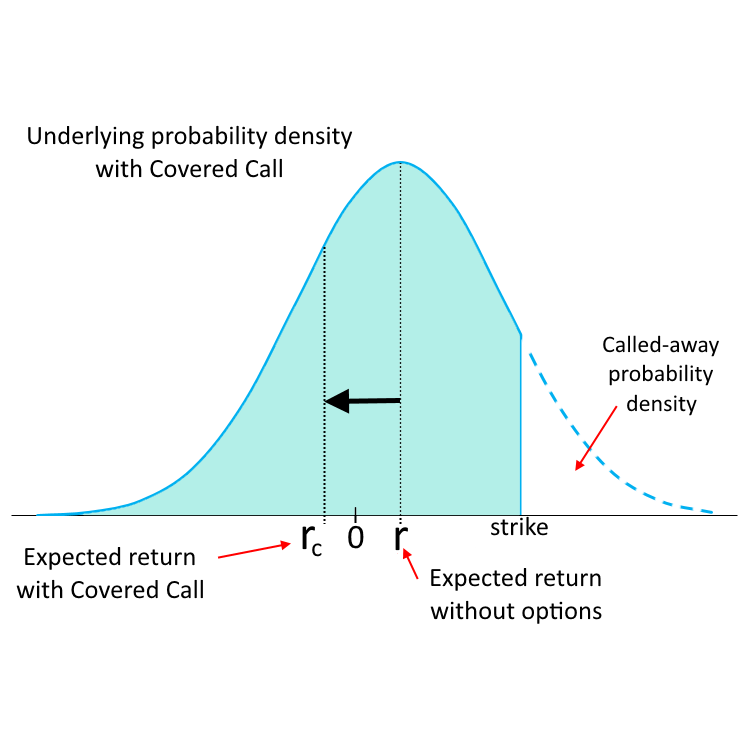

Theoretically, if an option seller bears this “drag”, a buyer, on the other hand, should benefit from removing this excessive volatility from his or her portfolio. In practical terms, with a long put option strategy as a hedge to a long equity portfolio, an investor can use the realized proceeds from put options at the time of a market crash as “dry powder” to buy more underlying assets at lower prices. This is also known as a “rebalancing bonus”, which is the opposite phenomena to the volatility drag.

In this research, we have studied whether put options overpricing is justified by this rebalancing bonus for a hedged portfolio. The results show that it is not. It turns out, there are no parameters (moneyness, DTE) of put options and put spreads that would make them an efficient hedge in the long run without predictions of market turmoils.

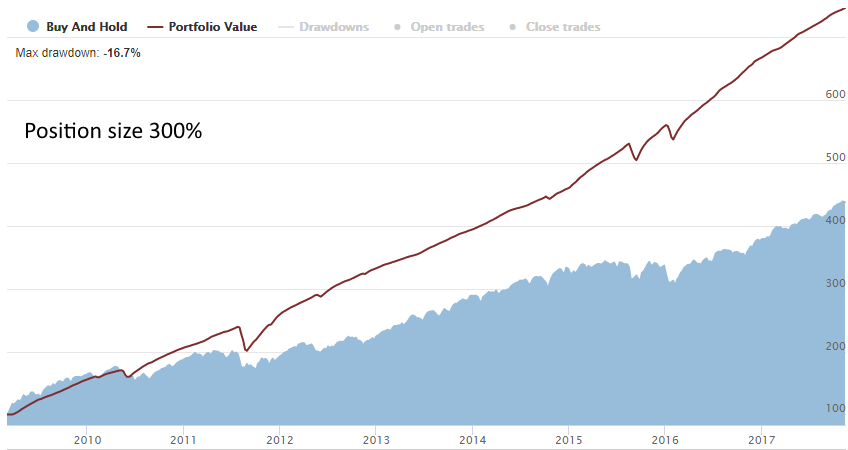

Covered Call strategy works great in downtrending or rangebound markets: short call legs have positive expected profit and decrease the overall portfolio volatility.

However, in the Bull Markets, it does not so look attractive, at the first glance: with uptrending price, the short call leg often expires in-the-money forcing the underlying security to be called out and not to participate in the market rise above the call strike. Overall, in bull markets, calls are underpriced on average and the short call strategies have negative expected profit.

This research is devoted to finding the answer to the question: can a Covered Call strategy be efficient in the Bull Market environment despite the fact that it has an expected profit less than a simple Buy&Hold of the underlying security.

The conclusion is yes, the Covered Call strategy, especially with calls in the ITM area, can be quite efficient due to the substantially lower volatility of returns and higher risk-adjusted performance. By means of leveraging, it is possible to achieve higher absolute return than with an outright Buy&Hold strategy while having the same risk level measured by standard deviation and maximum drawdowns.

There are various pieces of evidence exist confirming that put options on wide equity indices are permanently overpriced by the market. The excess demand for the long portfolio protection is believed to be the main reason for this.

This research conducted using the OptionSmile platform underpins that observation and confirms that a put options selling has abnormally high expected profit.

However, on the risk-adjusted basis, such a short put strategy does not look so attractive due to the high volatility of results and regular huge drawdowns: the Sharpe ratio of a put selling, even with limited risk (spread strategy), is not so attractive and does not differ significantly from the Sharpe ratio of the outright long position in the underlying security.

Therefore, that high profitability of puts should be considered as a volatility premium rather than a market inefficiency.

Covered Call is a popular strategy that is often considered as a source of additional income for a long-term equity investor. Writing OTM calls is supposed to be a conservative strategy an average investor can pursue to earn a supplementary gain in excess of the underlying assets return.

However, it turns out that the call overwriting against the major equity indices does not add any meaningful profit to the portfolio because almost all the premium collected from the short calls will eventually be lost in the form of not participating in the growth of the underlying security called-out in the cases of ITM expiration.

This research demonstrates that call options on equity indices are priced quite fairly on average (in the contrast to puts) and usually have expected profit/loss close to zero. Moreover, in the secular bull markets, they are mostly underpriced, and Covered Call imposes a drag on the portfolio performance.

Nevertheless, on a risk-adjusted basis, this strategy can be quite attractive, especially for the ITM calls selling.